On October 28, 2014

Share On:

The recently enacted Companies Act, 2013 ('the Act') is a landmark legislation with far-reaching consequences on all companies incorporated in India.

According to industry estimates the top 300 companies are audited by 10 firms and experts say the mandatory rotation within the next three years could trigger a lot of chaos and confusion. Similar challenges will exist for many companies. So it is very important for the companies and the auditing firms to have all the information organized and available at one place. These firms should start using Software to have all the information at one place. CADashboard tool will help the companies and auditing firms to effectively collaborate with each other and avoid future compliance challenges.

The recently enacted Companies Act, 2013 ('the Act') is a landmark legislation with far-reaching consequences on all companies incorporated in India. A part of the Act had already become effective with the notification of 98 sections in September 2013. Further on 26 March 2014, the MCA has notified most of the remaining sections. These sections have been notified to come into effect from 1 April 2014. The MCA has also published the several chapters of the related rules, and the remaining rules in respect of the notified sections are expected to be released by 31 March 2014. This is a landmark legislation that will have a wide ranging impact on corporate India.

The Act in a comprehensive form purports to deal with various aspects of corporate India and Indian companies will have to closely examine these developments to develop a clear strategy at ensuring compliance per the new requirements.

Key Highlights

Appointment and Variations regarding Directors & Key Managerial Personnel:

- Appointment

- Certain Companies, as may be prescribed, to mandatorily appoint company secretary.

- Appointment of at least one women director on the board of prescribed classes of companies has been made mandatory.

- Appointment of at least one director resident in India, i.e., a director who has stayed in India for at least 182 days in the previous calendar year, is made mandatory for all companies.

- Key Managerial Personnel

- Company Secretary included within the definition of Key Managerial Personnel.

- No company can have both Managing Director and Manager at the same time.

- Every company belonging to such class or description of companies as may be prescribed, to have managing director, or chief executive officer or manager and in their absence, a whole-time director, company secretary and chief financial officer.

- Status of Independent Director

- Nominee director cannot be regarded as Independent Director.

- Maximum term of Independent Director has been restricted to five years at once subject to a maximum of two such terms

- The independent director is not entitled to stock option and may receive remuneration by way of fee and profit related commission as approved by members.

- Role or functions of independent directors is expanded.

- Directorships

- Maximum number of directors has been increased from twelve (12) to fifteen (15) directors. Further no Central Government approval is required to increase the maximum no. of directors beyond fifteen (15). Shareholders of companies may do so by passing a special resolution.

- A person can hold directorship of up to 20 companies, of which not more than 10 can be public companies.

- Meeting of Board and its Powers:

- A notice of not less than 7 days in writing is required to call a board meeting. The notice of meeting to be given to all directors, whether he is in India or outside India by hand delivery post or electronic means.

- A notice of not less than 7 days in writing is required to call a board meeting. The notice of meeting to be given to all directors, whether he is in India or outside India by hand delivery post or electronic means.

- Every Listed Company and such other company as may be prescribed shall have an Audit Committee.

- The central government permission under section 295 and section 372A of Companies Act, 1956 is dispensed with.

- Following committees of the Board made mandatory for listed and prescribed classes of companies:

- Audit committee

- Stakeholder relationship committee

- Nomination and Remuneration committee

- Corporate Social Responsibility committee

- Accounts & Audit:

- Books of accounts can be kept in electronic form also

- The term balance sheet & profile and loss accounts are collectively termed as financial statement.

- The Act provides for re-opening or re casting of Books of Accounts at the instance of regulatory authorities. The financial statements can be revised at specified situations.

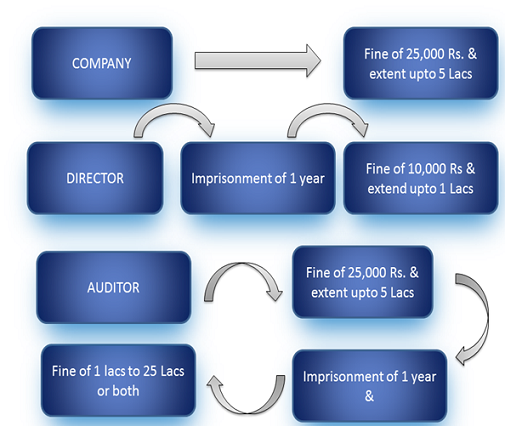

- No listed companies shall appoint.

- an individual as auditor for more than one term of five consecutive years, and

- an audit firm as auditor for more than two terms of five consecutive years.

- Shareholders are at liberty to decide by passing resolution that audit partner and the audit team, be rotated every year.

- Auditor shall not provide directly or indirectly the specified services to the Company, its Holding and subsidiary companies.

- Auditor shall not provide directly or indirectly the specified services to the Company, its Holding and subsidiary companies.

- Financial year will be uniform for all companies i.e., April-March.

- Related Party Transactions

- Scope of related party transactions has been widened and definition of relatives has also been enlarged and replaced with definition of “related party”.

- Clause 188 of the Act which carries provisions regarding related party transactions, combines existing sections 297 and 314.

- The Act provides for re-opening or re casting of Books of Accounts at the instance of regulatory authorities. The financial statements can be revised at specified situations.

-

Central Government Approval has been done away with. Every related party transaction to be disclosed in Board’s report along with the justification.

- Approval in the Board is mandatory and also require prior shareholders approval for specified share capital and prescribed amounts.

- Inspection & investigation:

- The provision for establishment of Serious Fraud Investigation Office (SFIO) by the Central Government is another significant feature of the Act.

- SFIO is empowered to arrest in respect of certain offence involving fraud.

- Corporate Social Responsibility (CSR):

- Formation of CSR Committee has been made mandatory for a company having net worth of Rs. 500 crore or more, or turnover of Rs.1,000 crore or more or net profit of Rs. 5 crore or more during any financial year.

- Such company shall spend, in every financial year, at least 2 % of the average net profits of the company made during three immediately preceding financial years, in pursuance of its Corporate Social Responsibility Policy (CSRP).

- Compromises, Arrangement and Amalgamation:

- The Act allows cross border mergers

- Separate provision for merger between two small companies or holding and wholly owned subsidiary

-

- Any valuation of shares / assets etc. required to be performed by a Registered Valuer

- National Company Law Tribunal (NCLT) :

- NCLT replaces the High Court, CLB. The same shall consists of Judicial and Technical members, as Central Government may deem necessary, to exercise and discharge the powers and functions conferred including approval of merger, corporate reorganization, capital reduction, extension of financial year etc.

- Every proceeding presented before the Tribunal shall be dealt with and disposed of within 3 months from the date of commencement of proceeding before the tribunal.

E-Governance - The Act required proposed for various company processes like maintenance and

inspection of documents in electronic form, option of keeping of books of accounts in

electronic form, financial statements to be placed on company’s website, holding of

board meetings through video conferencing/other electronic mode; voting through

electronic means

E-Governance - The Act required proposed for various company processes like maintenance and

inspection of documents in electronic form, option of keeping of books of accounts in

electronic form, financial statements to be placed on company’s website, holding of

board meetings through video conferencing/other electronic mode; voting through

electronic means

Because of the requirement of E-Governance and mandatory rotation of audit firms, these firms should start using Software to have all the information at one place. CADashboard will help the companies and auditing firms to effectively collaborate with each other and avoid future compliance challenges.

CADashBoard is one such platform which chartered accountants can use.

Comments